Cash-In Refinance

Here's an interesting thought. Instead of pulling money out of your equity when refinancing your home, consider putting some cash into your equity. The strategy would be to get a considerably lower rate and a shorter term than 30 years. It will pay off your mortgage sooner, build equity faster and save lots of money in interest.

|

|

If you have some extra cash available, this might be very atteractive compared to what your are earning currently on those savings.

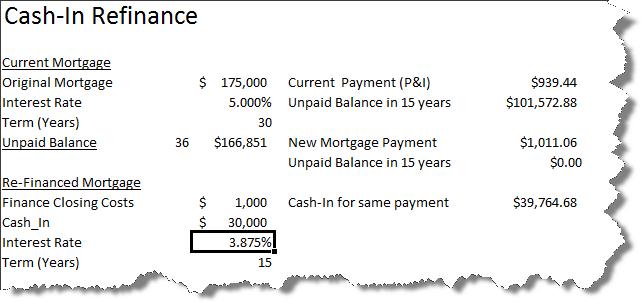

In the example below, the current mortgage is at 5% for 30 years with payments of $939.44. The owner can refinance for 15 years at 3.875%. If he puts $30,000 into the refinance, his payments will be slightly more than the current $1,011.06 but the mortgage will be paid off in 15 years. At that same point, if he keeps the current mortgage, his unpaid balance will be $101,572.88.

In order to have the same payments as the mortgage he is refinancing, he'll need to add $39,764.68 to the refinance.

If you have a goal to get your home paid off and you have some funds available, a Cash-In Refinance may be just the strategy for you.